Jon Gosselin may have purchased a few too many Ed Hardy shirts back in the day, because he’s been hit with a tax lien by the IRS – to the tune of $39,000. Can you get a refund on hair plugs? The former THG fixture owes that much from just 2009 – the year Jon and Kate Gosselin split, and the last year he likely had any sort of stable income. Since then, he’s kinda faded into obscurity. Despite all the money he made from celebrity gossip interviews and photos that year, according to papers filed in Berks County, Pa., Jon is still delinquent. TMZ was not able to get a quote from Jon. Think is flip phone is still in service? Given that Jon works a totally normal job again, and has eight kids to support, 39 grand might be tougher to scrounge up than back in his TLC heyday. Let’s hope he saved and invested well pre-divorce drama. We’re sure he stashed his earnings away while the gettin’ was good. Actually we’re not. We don’t know him personally, but we sincerely doubt it.

Thursday, January 10th, 2013 at 9:01 am PST… So Justin Timberlake mysteriously Tweeted last night, sending fans into a frenzy over what would the artist would announce at that time. And now we know: he’s ready to make music again! “I don’t want to put anything out that I don’t love,” Timberlake explains in the following video. “You just don’t get that every day. You have to wait for it.” When will we actually hear new songs from JT? It’s unclear. But sexy WILL be back on the scene at some point, people. Watch this cool video now and place your d-ck in a box in celebration… Justin Timberlake Album Announcement

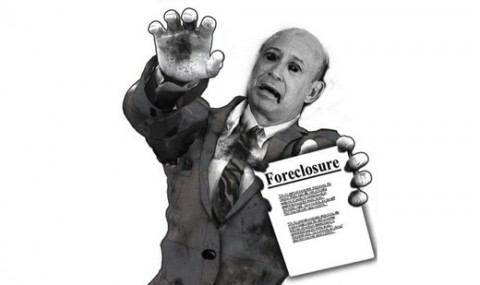

Zombie foreclosures. This bizarre term refers to a bizarre, little-known but very real horror of the U.S. housing bust that is crippling homeowners coast to coast, six years in. Thousands are finding themselves legally liable for houses they didn’t know they still owned after banks decided it wasn’t worth their while to complete foreclosures. With impunity, banks walk away from foreclosures much the way some homeowners walked away from their mortgages when the housing market first crashed. “The banks are just deciding not to foreclose, even though the homeowners never caught up with their payments,” says Daren Blomquist, vice president at RealtyTrac. Since 2006, 10 million homes have fallen into foreclosure, a number that in earlier, more stable times would have taken nearly two decades to reach. Of those foreclosures, more than 2 million have never come out. In cases where homeowners moved out after receiving notice of a foreclosure sale, thinking they were leaving the house in bank hands, we see the zombie situation. Dozens of housing court judges, code enforcement officials, lawyers and other professionals involved in foreclosures say these titles number in the many thousands. No national databases track zombie titles. “There are thousands of foreclosures in limbo, just hanging out there, just sitting, with nothing being done,” says Cleveland Housing Court Judge Raymond Pianka. The surge is due largely to homes vacated by people who fled before an imminent foreclosure sale, only to learn later that they remain legally responsible for their house. When people move out after receiving a notice of a planned foreclosure sale and the bank then cancels, municipalities are left to deal with the mess. Some spend public funds on securing, cleaning and stabilizing houses that generate no tax revenue. Others let the houses rot, as we’ve seen many times. In at least three states in recent months, houses abandoned by owners and banks alike have exploded because the gas was never shut off. Unsuspecting homeowners nationwide have had their wages garnished, their credit destroyed and their tax refunds seized – all due to zombie titles. They’ve opened their mail to find bills for back taxes, graffiti-scrubbing services, demolition crews, trash removal, gutter repair, exterior cleaning and lawn clipping. At their front doors they’ve encountered bailiffs brandishing summonses. In some cities, people with zombie titles can be sentenced to probation – with the threat of jail if they don’t bring their houses into compliance. If you think this could be happening to you, or for more information on this dubious but very real situation, continue reading this foreclosure explanation .

The bad news is, if you already lost your home you’re not gonna get more than two stacks for your sorrows… The good news is, if your loan is bigger than what your house is worth, the bank has to restructure your loan and help you out! Here’s the details: Federal officials announced Thursday that 49 states have accepted a $25 billion foreclosure-abuse settlement with the five largest mortgage lenders — a deal that primarily helps underwater homeowners but pays just $2,000 to those already wrongly foreclosed upon. The bulk of the deal requires the banks to reduce some loans and refinance mortgages for underwater borrowers. Oklahoma was the lone holdout to the agreement. President Obama described the deal as a “landmark settlement” that would “begin to turn the page on an era of recklessness” while speeding relief to hard-hit homeowners. It is the biggest settlement involving a single industry since a 1998 multistate tobacco deal. Under the agreement, five major banks — Bank of America, JPMorgan Chase, Wells Fargo, Citigroup and Ally Financial — will reduce loans for nearly 1 million households. Those who lost their homes to foreclosure are unlikely to get their homes back or benefit much financially from the settlement. For those improperly foreclosed upon, the banks will cough up checks of $2,000 to about 750,000 Americans. The banks will have three years to fulfill the terms of the deal. The deal was geared more toward homeowners who are struggling to make payments now, yet still have possession of their homes. The agreement requires the banks to commit a staggering amount of money toward changing loan terms. At least $10 billion will go toward reducing the principal for borrowers who are delinquent or underwater borrowers at risk of default. At least $3 billion will go toward refinancing. Other payments will go toward state governments, and the federal government, to “repay public funds lost as a result of servicer misconduct,” according to the Justice Department. Obama, noting the damage the housing bubble did to the broader U.S. economy, said no single action would heal the housing market. But he described the settlement as an important step, one which would address alleged abuses by mortgage lenders — like using fake signatures in the foreclosure process. “These practices were plainly irresponsible, and we refused to let them go unanswered,” Obama said. All but one of the 50 states agreed to the deal. Oklahoma, the lone holdout, will receive no money. That state’s attorney general had opposed the massive fine included in the settlement, and reportedly was concerned the penalty went beyond the scope of the original investigation. Attorney General Eric Holder said the deal would “hold mortgage servicers accountable for abusive practices.” The conditions will be overseen by Joseph A. Smith Jr., North Carolina’s banking commissioner. Lenders that violate the deal could face $1 million penalties per violation and up to $5 million for repeat violators. During the financial and housing crisis, home values sank and millions edged toward foreclosure. Many companies processed foreclosures without verifying documents. Some employees signed papers they hadn’t read or used fake signatures to speed foreclosures — an action known as robo-signing. Under the deal, the 49 states have said they won’t pursue civil charges related to these types of abuses. Homeowners can still sue lenders in civil court on their own, and federal and state authorities can pursue criminal charges. Bank of America will pay the most to borrowers as part of the deal — nearly $8.6 billion. Wells Fargo will pay about $4.3 billion, JPMorgan Chase will pay roughly $4.2 billion, Citigroup will pay about $1.8 billion and Ally Financial will pay $200 million. This does not include $5.5 billion in federal and state payments. The deal also ends a separate investigation into Bank of America and Countrywide for inflating appraisals of loans from 2003 through most of 2009. Bank of America acquired Countrywide in 2008. The banks and U.S. state attorneys general agreed to the deal late Wednesday after 16 months of contentious negotiations. New York and California came on board late Wednesday. California has more than 2 million “underwater” borrowers, whose homes are worth less than their mortgages. New York has some 118,000 homeowners who are underwater. In addition to the payments and mortgage write-downs, the deal promises to reshape long-standing mortgage lending guidelines. It will make it easier for those at risk of foreclosure to make their payments and keep their homes. The settlement would apply only to privately held mortgages issued from 2008 through 2011. Banks own about half of all U.S. mortgages — roughly 30 million loans. Seems like Barry O meant what he said in his State of the Union Address after all. It’s not gonna make him too popular with the Wall Street cats, but he prolly lost that battle a long time ago. Hopefully this helps get America closer to where we need to be. Source More On Bossip! For The Conspiracy Theorists: A History Of Alllll The “Evidence” That Bey Was Never Carrying A Gut Full Of Anything Ho Sit Down: The Most Hated Sports Wives And Girlfriends Of All Time Are You My Daddy? Khloe Heats Up The DNA Debacle By Posing With Kris Jenner’s Ex-Jumpoff Hairdresser The Side-Eye: Ne-Yo Makes It Rain In An Atlanta Strip Club With His Baby Mama To Convince Us That He Isn’t Rooty-Tooty Fresh And Fruity [PICS]

Victor Davis Hanson and Kyle Smith explore two upcoming bailouts, one directed at state governments – and therefore at the public employee unions whose lavish contracts threaten to bankrupt a number of state treasuries – and the other at homeowners who can’t afford their mortgages. “What did you expect?” asks Hanson . Progressive culture, where ads blare hourly about skipping out on credit card debt, shorting the IRS, and walking away from mortgages, did the public employee unions really think they were exempt from a Chrysler-like renegotiation? In the age of Obama, there is no real contractual obligation: everything from paying back bondholders to fixing a BP penalty is, well, “negotiable.” When the money runs out, the law will too. Law? There is no law other than a mandated equality of result. “That’s right,” Smith notes : If you bet badly in the housing-market casino of the Aughties, the government is thinking of refunding some of your chips so you can play again. You may have heard something about a sub-prime real-estate bubble that popped and nearly took down the financial system with it? President Obama wants to double down. Are we starting (continuing) to see a pattern here?

Did you know that traders at the troubled investment bank are legendary health nuts? It’s true! So could a fastfood eating contest between 10 mortgage traders at the firm have lead to the housing market collapse of 2007? More